🏡💚 The insurance doom loop and politics of solidarity

As a renter, I almost never think about home insurance in my personal life. But mention insurance to any homeowner, and they almost always have something to say.

That’s because home insurance rates have been skyrocketing. Some reports have estimated a 21% increase in home insurance costs statewide this year, but the costs can vary dramatically by location and insurance policy. Numerous individual anecdotes describe rate increases doubling or tripling overnight.

The home insurance crisis has gained even more attention in recent years as some of the biggest insurance providers have begun refusing to cover policies for huge areas of the state. Thousands of Los Angeles homeowners were dropped from their insurance coverage in the year before the Eaton and Palisades fires.

The reason for this is simple: climate change, and the disasters fueled by it. Increasingly frequent and extreme disaster events are causing more payouts, pushing insurance companies to raise rates for everyone. And a growing number of insurers are looking at climate risky areas and just deciding they’re not worth covering at all.

So far I don’t think that connection between insurance hikes and climate change is being made for most people. We often talk about how the long-term cost of inaction on climate change will be much worse than the upfront costs. This is climate change literally hitting people’s monthly budget, and they probably don’t even know it.

I’ve been wondering why that is. Unlike a lot of other messages around climate change, this one is really straightforward. You don’t need to walk someone through multiple convoluted steps, or get too sciency. The reasoning is a 1:1 direct line: your insurance costs are going up because private insurance companies know that climate change is threatening more and more homes.

For the climate left, I think there are a few main reasons we don’t focus on insurance: (1) just saying the word ‘insurance’ can make most people’s eyes glaze over, (2) we don’t have a clearly identified solution, and (3) the most directly impacted people are homeowners, which are typically not the constituency we are trying to organize. But by not engaging on this, we are missing out on an opportunity to politicize the issue and connect it to the cost of living crisis that is affecting millions of people.

And the thing is, it’s not just impacting homeowners. These costs also impact renters, but they just get passed down more indirectly through rent increases where the reason for the increase is obscured. Tenants don’t see a line item in their monthly rent that says ‘this part goes to cover the rising cost of insurance’ — they just see their rent going up.

Affordable housing developers are also raising the alarm about the acute impacts insurance costs are having on the affordable housing sector. In San Francisco, one affordable housing project reported an insurance increase from $58,000 for their policy in 2022 to $171,000 in 2023 (nearly 300% increase). In Los Angeles, a permanent supportive housing project saw an increase from $94,000 to over $519,000 — a 450% increase.

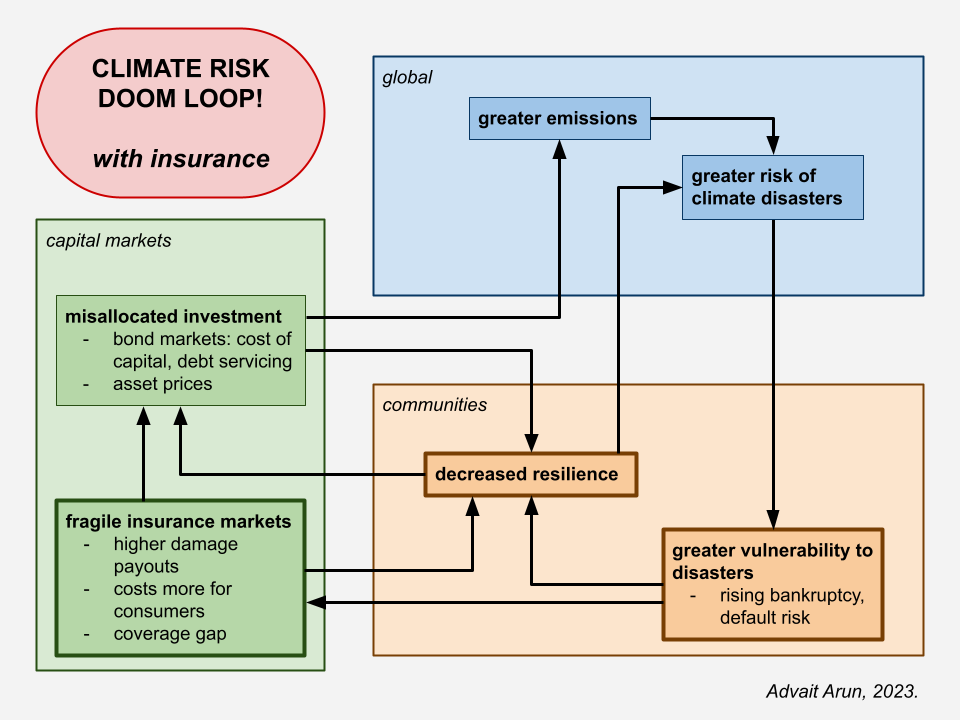

Above and beyond the challenges of home insurance costs, there is a much greater looming threat. It’s not so much that things will just continue down this path, but that it will begin a doom loop that exponentially exacerbates all inequities.

As Advait Arun points out in that article, insurance markets are only a subordinate part of a deeply unequal economic system, one where capital investment is moving away from “riskier” or “less resilient” communities while still investing deeply in fossil fuel infrastructure. As others have pointed out, this system of disinvestment and withdrawing services from places with high climate risk also closely tracks formerly redlined areas.

This doom loop has very specific consequences for the housing market, which raises the specter of the 2008 financial crisis. Senator Sheldon Whitehouse described this succinctly in a congressional hearing earlier this year: “Climate risk makes things uninsurable. No insurance makes things unmortgageable. No mortgages crashes the property markets. Crashed property markets trash the economy.”

I’m not saying all of this just to be seasonally spooky or cause more climate anxiety. Rather, I want to make the case that we’re missing out on a critical opportunity to motivate and build support for urgent climate action. And as wonky as insurance appears, at its very core it’s about the concept of solidarity. In the face of climate change, what responsibility do we have toward one another?

As described by Climate + Community Institute’s report that bears the name, the issue of insurance and climate change is fundamentally a question of shared fates. Right now, we leave that answer up to private, for-profit insurance companies and hope that they can price signal our way toward resilience. And when those companies decide not to cover some homes, we pick that up through the state’s FAIR plan — the insurer of last resort that provides somewhat of a safety net, while also essentially being set up to fail by concentrating the riskiest policies by design.

One of the many obvious problems with price signaling as a strategy is that housing is not a “liquid” asset that is easily movable. The fact is, entire communities already exist in areas that have become higher risk due to no fault of their own. We’re going to need to make hard decision about a managed retreat, and how to build back from disasters, but we also need to resist the all-too-easy narrative of individualism: why should I pay for someone else’s bad decision on where to live? In the face of climate change, we need a politics of solidarity — not just as a moral principle, but because it will require enormous collective action to address the collective threat. The only way to do something is to do it together.

In California we have a relatively unique set of opportunities to politicize this issue and talk to people about it. Due to Prop 103 (which passed in 1988), we are one of 11 states with a publicly elected Insurance Commissioner role. The current Insurance Commissioner, Ricardo Lara, is termed out after serving 8 years, so there’s an open race for that position in 2026. We already know that state Senator Ben Allen and former state Senator Steven Bradford are both running, with others mulling throwing their hat in the ring. In a year that will have a lot of attention sucked up by the Governor’s race, Congressional seats, and ballot measures, this is an under-the-radar elected position that nonetheless has the potential to play a huge role in shaping the state’s response to the insurance crisis moving forward.

No single issue is going to create a political vision. Insurance certainly won’t do that, but neither will something like universal health care, green social housing, humane immigration policy, or taxing the rich. The challenge is how to create a common thread through all of them that bring coherence to the ways people see what’s happening in the world, and helps them believe in a different path forward. To me, the insurance crisis—and frankly all of the other issues I just listed—is fundamentally about our societal approach to the concept of solidarity. Will we leave each other to our separate fates? Or will we stand together across difference for the common good?

Water’s rising — what are we going to do? Source: Phenomenal World

WHAT WE’RE READING

Insurers of Last Resort: Why Today’s FAIR Plans Need a Redesign to Address the Home Insurance Crisis (Climate + Community Institute)

Insurance in the Polycrisis (Phenomenal World)

Lessons From Redlining: How We Can Prevent Climate-Driven Insurance Discrimination (Shelterforce)

You Can’t Have Social Housing Without Building Housing (Jacobin)

What Would It Take To Make Community Ownership The Rule, Not The Exception? (Shelterforce)

Feel free to reply any time! I always enjoy hearing from people and getting any feedback/questions/additional thoughts.

We send these out on a somewhat weekly basis. If you don’t want to get these newsletters, feel free to unsubscribe below. If you know someone that would be interested, send me their email, or you can forward this along to them and they can use this link to subscribe.